The Facts Are Friendly

People and startups grow by facing reality.

- The facts are always friendly, every bit of evidence one can acquire, in any area, leads one that much closer to what is true.

- Why does Sam Altman need $7 trillion?

- Should a semiconductor company be worth more than the energy sector?

- We discuss Sora, a new text-to-video AI model from OpenAI.

🙏 My work is reader–supported. You can get a membership here!

📣 Before Growth has grown through word of mouth. Want to help? Share it on Twitter here, Facebook here, or LinkedIn here.

📚 My new ebook Generative AI in Product Design offers case studies on AI and just enough theory for you to build your next app with gen AI. Get your copy here!

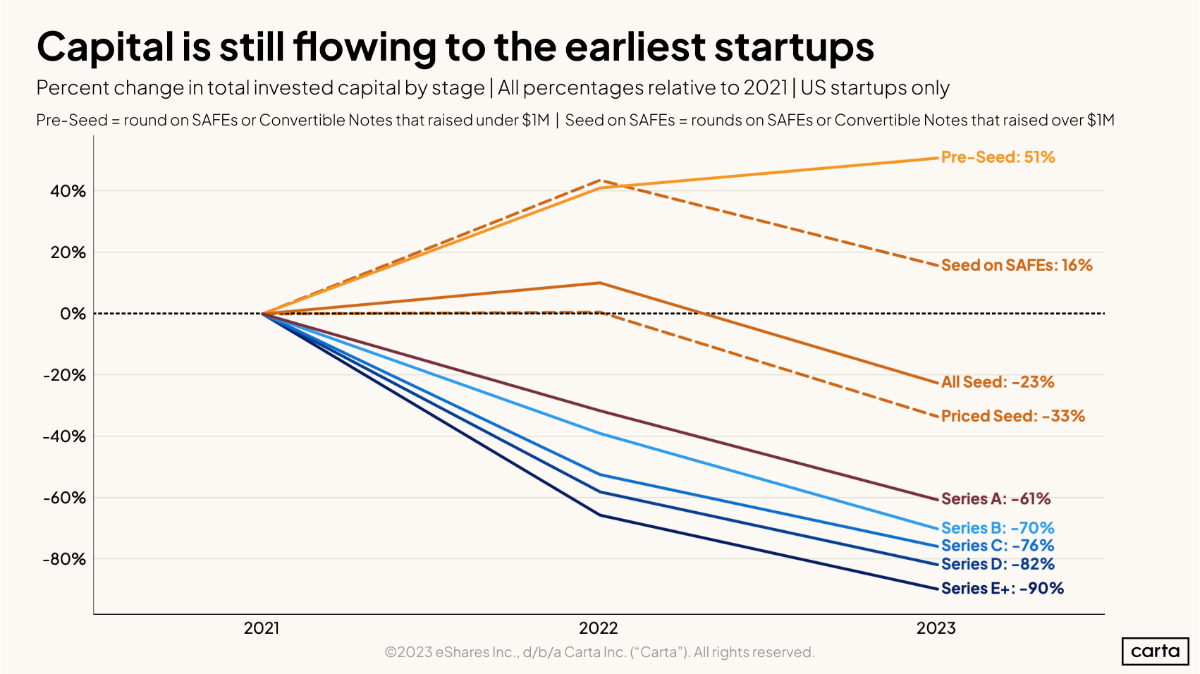

Funding… funding finds a way

Carta’s new research points out that overall investment has dipped in nearly every stage of venture funding when you look at 2023 compared to 2021. Yet, when you dive deeper into the numbers, something interesting pops up. Money flowing into pre-seed companies—which means those raising under $1 million through SAFEs or convertible notes—has actually jumped over 50% from 2021.

However, it’s worse for companies in the mid-to-late stages where the downturn continues with little improvement. To get back on track and push through the financial gloom in 2024, there’s a real need for a boost in late-stage venture investments.

Why does Sam Altman need $7 trillion?

Scott Alexander recently shared some intriguing thoughts on the scaling up of GPTs, explaining why Sam Altman of OpenAI is looking for ways to dramatically increase the world’s computing capacity. According to Alexander, GPT-6 might need about 10% of the world’s computers, enough energy to rival a large power plant, and more training data than we currently have access to. This could mean setting up a data center as big as a small town, powered by an extensive setup of solar panels or maybe a nuclear reactor. Alexander also mentioned that, as things stand, creating GPT-8 seems impossible. Even if we make leaps in synthetic data, harness fusion power, and take over the entire semiconductor industry, it still wouldn’t be enough to make it a reality—not without a breakthrough.

This insight also seems to suggest that OpenAI’s current strategy revolves “just” around linear scaling. There are no hidden projects in the pipeline. The focus remains on developing larger models and making incremental improvements—until we devise a more efficient architecture. And there’s definitely room for improvement; after all, human brains achieve similar or better results without needing as much data or training.

Should a semiconductor company be worth more than the energy sector?

Still on the subject of chips, Nvidia’s share price is hovering around $700 as of this writing, making it more valuable than the entire S&P 500 Energy Sector with a market cap close to $1.8 trillion. I recently chose to invest in it, along with a few other companies, and then found out that a good portion of financial Twitter seems to think the stock is in a bubble. Lucky me. As always. But is it really? (Knowing my luck, probably yes.)

To be honest, I’ve got no idea. I’m not a professional investor, so take my words on stocks with a grain of salt and do your own research. I’m just sharing my observations from the last couple of months. Some folks are drawing parallels between Nvidia’s rapid growth and Cisco’s during the dot-com bubble, which isn’t a far-fetched comparison. Both companies provided the infrastructure for new trends like the internet or AI. Early in the growth curve of a trend, it makes sense to back infrastructure providers since the eventual winners aren’t yet clear, and in many cases, haven’t even emerged. But there’s always money to be made by selling shovels during a gold rush.

Other analysts argue that chart comparisons can be manipulated to prove anything, depending on your starting point. They note that Nvidia’s stock would need to triple in the next 433 days to reach the levels seen during the dot-com bubble. Some even set a price target of $1,200 for it. However, if Nvidia's price were $1,200 today, its valuation would surpass Apple’s… You can see why I’m feeling anxious, right?

No matter your thoughts on Nvidia, it’s clear the market is showing some bubble-like behavior right now. Supermicro, under the ticker $SMCI, just experienced a 20% drop in a single day from its peak, now trading at around $800 a share. To put that in perspective, it was trading at about $100 per share in early 2023, marking an 800% increase in just over a year. Yeah, reasonable, nothing to see here. What does Supermicro do? To be honest, I wasn’t familiar with the company until I started digging into this. They sell servers, apparently. And in 2024, is that really worth so much? Probably not—but in June 2023, there was a spike in demand for Supermicro’s AI systems optimized for large language models, thanks to NVIDIA chips. So, that “explains” the surge…

If that doesn’t scream bubble, then I’m not sure what does.

There are other telling economic signs too. Cash has become a more appealing option than stocks, which means there’s less reward for taking risks and more for just holding onto cash. This scenario last played out just before the dot-com crash. Currently, we’re witnessing an extraordinary wave of insider selling. Jeff Bezos just offloaded shares of Amazon valued at $6 billion, while Mark Zuckerberg sold $840 million worth of Meta shares, Netflix’s CEO sold $40 million, and Palantir insiders sold another $35 million. The last time we saw this level of selling activity was in 2022, right before the Nasdaq took a 30% hit. Meanwhile, Japan and the UK are facing recessions, Germany narrowly avoided one despite its economy shrinking by 0.3% in 2023, and the European Union's economy technically grew by 0.1% last year—but yeah, it’s not really that optimistic…

Though it’s a bit off-topic for this newsletter, I know a lot of us are into tech investments, so I thought I’d share how my thinking on the matter is shaping up.

Bits

- Sora is an AI model developed by OpenAI that’s capable of generating realistic video from text prompts. It’s pretty mind-blowing. Definitely give it a look if you haven’t yet, though I’d be surprised if you haven’t come across it already. It’s blowing up on Twitter. There’s not much more I can say right now since it’s still not widely available to the public.

- Zuckerberg believes that glasses will become the mobile devices of the future, while headsets are set to be the laptops of the future. Yeah, I can see that happening.

- OpenAI is currently testing a feature that allows ChatGPT to recall things from your chats, aiming to make future conversations more useful. This is actually something I suggested in my blog post about context windows. So, if anyone from OpenAI is reading this, I’m open to sharing more insights and ideas!

- A mob recently wrecked a driverless Waymo car in San Francisco. For more than ten years, I’ve toyed with a story idea about riots breaking out in the city, sparked by massive job losses among two key groups: drivers, due to autonomous vehicles, and retail employees, because of self-checkout grocery stores. This incident would serve as a gripping start to the tale. To make the story even more relevant today, I’d include the angle of office workers being laid off because of advancements like ChatGPT. But it’s all just a story… isn’t it?

- CrewAI is a framework designed to manage role-playing, autonomous AI agents. It encourages collaborative intelligence, enabling these agents to work together smoothly to handle complicated tasks.

- Air Canada has found itself in a position where it needs to stick to a refund policy that was unintentionally invented by its chatbot. It's a good reminder that ChatGPT started off as a research demo, largely because the technology it’s built on can still be a bit unreliable and not always prepared for widespread deployment.

- A review of Walter Isaacson’s “Elon Musk”. There’s a lot in there that didn’t vibe with me, but I do echo the sentiment that Isaacson seems to ignore the truly fascinating aspects of leaders like Musk or Steve Jobs, who also had a biography he wrote. For example, the part where Musk’s first son passes away is quickly covered and then it’s straight back to rocket science, human emotions be damned. That’s actually where I started to lose interest in the book. “Steve Jobs” felt similar in that respect. If you’re looking for a deeper dive when it comes to Apple’s founder, I’d point you towards Brent Schlender’s “Becoming Steve Jobs,” which is much better. It genuinely attempts to paint a full picture of who Jobs was, capturing both his flaws and his brilliance, instead of reading like a boring history book.

Today’s topic

Imagine two founders.

The first entrepreneur is new to this and hasn’t launched a startup before. They’ve managed to secure their first investment meeting, but the fact that they don’t even have a hundred users is making them feel insecure. In an attempt to make things look better, they tweak the numbers in their pitch deck, making it seem like all their users are actively engaging every month. Or they stretch the truth in a different slide—maybe not exactly a lie, but more like they leave out a tiny detail or phrase something in a way that’s a bit more positive than it really is. They’re hoping that by the time anyone double-checks these figures, the startup will have grown to match these numbers anyway. No harm done.

The second founder comes with experience, feeling confident from a successful exit in their past venture. Just like the first, they’re at the beginning stages, but their numbers are even less impressive, with only tem daily active users. A few days after the first founder, they present the raw numbers to the same venture capital firm.

Who do you think is more likely to get funded?

The second founder has the edge. At this early phase, investing in people is the smart move. So, if someone with a proven track record approaches you, it’s likely you’ll invest. They’ve succeeded before, suggesting they can do it again. However, given the abundance of capital in these funds, and considering that early-stage VCs and startup accelerators often discover relatively unknown talents and fund their ideas, the less experienced founder isn’t necessarily at a disadvantage.

However, following the next investment committee meeting, it turns out that the less experienced founder does, in fact, end up losing. Why?

VCs and other people in power tend to get really good at spotting when someone’s not being completely honest with them, especially if it’s to get something they want. If they take a closer look, they’ll realize the foundations aren’t that strong. Having a small group of users who are really into what you’re doing is way better than “having” lots of users who look like they hardly pay attention. The second founder can easily share stories about how their project made a real difference for each of their users, and even provide references. The first founder, on the other hand, might not have those kinds of stories to tell and could end up bending the truth too far by inventing them, too, crossing further into outright dishonesty. Like a death spiral.

Fame, money, and ambition can lead people to make some questionable choices. It’s not by chance that shows like “Silicon Valley” on HBO highlight manipulating investors, employees, and the press as a common issue in startup culture. I don’t think it’s a deep-rooted part of our culture, but we do see it pop up now and then, with cases like FTX grabbing headlines. When there’s a ton of money at stake, it’s easier to drift away from your original values. And just to be clear, I’m not saying that all first-time founders are out there juicing the numbers; it’s just a story that a friend shared with me, told anonymously.

Personally, I strongly believe that the truth always surfaces eventually. The situation with FTX and other similar cases proves that point. In our story, treating the truth as something to be avoided actually backfires, because the founder ends up not getting the investment anyway. As Dostoyevsky wrote, “Your worst sin is that you have destroyed and betrayed yourself for nothing.”

I get where the first founder is coming from. Even in situations at work that aren’t worth billions of dollars, if I feel like I messed up, there’s sometimes this little voice in my head whispering, “Maybe we can just... hide it?” Nobody wants to look bad or get the blame when things go bad. So if I keep quiet, maybe no one will notice. Maybe I can tweak the truth just a bit so it doesn’t look like my fault. I think everybody hears this voice from time to time. But it's never worth listening to it. Being open and simply dealing with the issue is always the better route. If you end up losing your job over being honest, the worst case scenario, then maybe that’s for the best. In my experience, working for someone who can’t handle the truth comes back to bite you eventually. They will use that against you sooner or later.

Carl Rogers, the famous psychotherapist, once said, “The facts are always friendly, every bit of evidence one can acquire, in any area, leads one that much closer to what is true.” He believed that facing reality is how people grow. Often, people might cherry-pick information that aligns with their preferred viewpoint. While this might feel comforting, it can lead to a denial of reality or attempts to twist it—as we’ve seen in our story. Rogers argued that we should embrace new information, even if it proves our previous beliefs wrong or makes us uncomfortable, because truth has a healing power that helps us move forward.

I agree. Don’t be afraid.

The future of tech, direct to your inbox

Discover the next generation. Subscribe for hand-picked startup intel that’ll put you ahead of the curve, straight from one founder to another.

{kind=link}

{kind=link}